💡 In one sentence

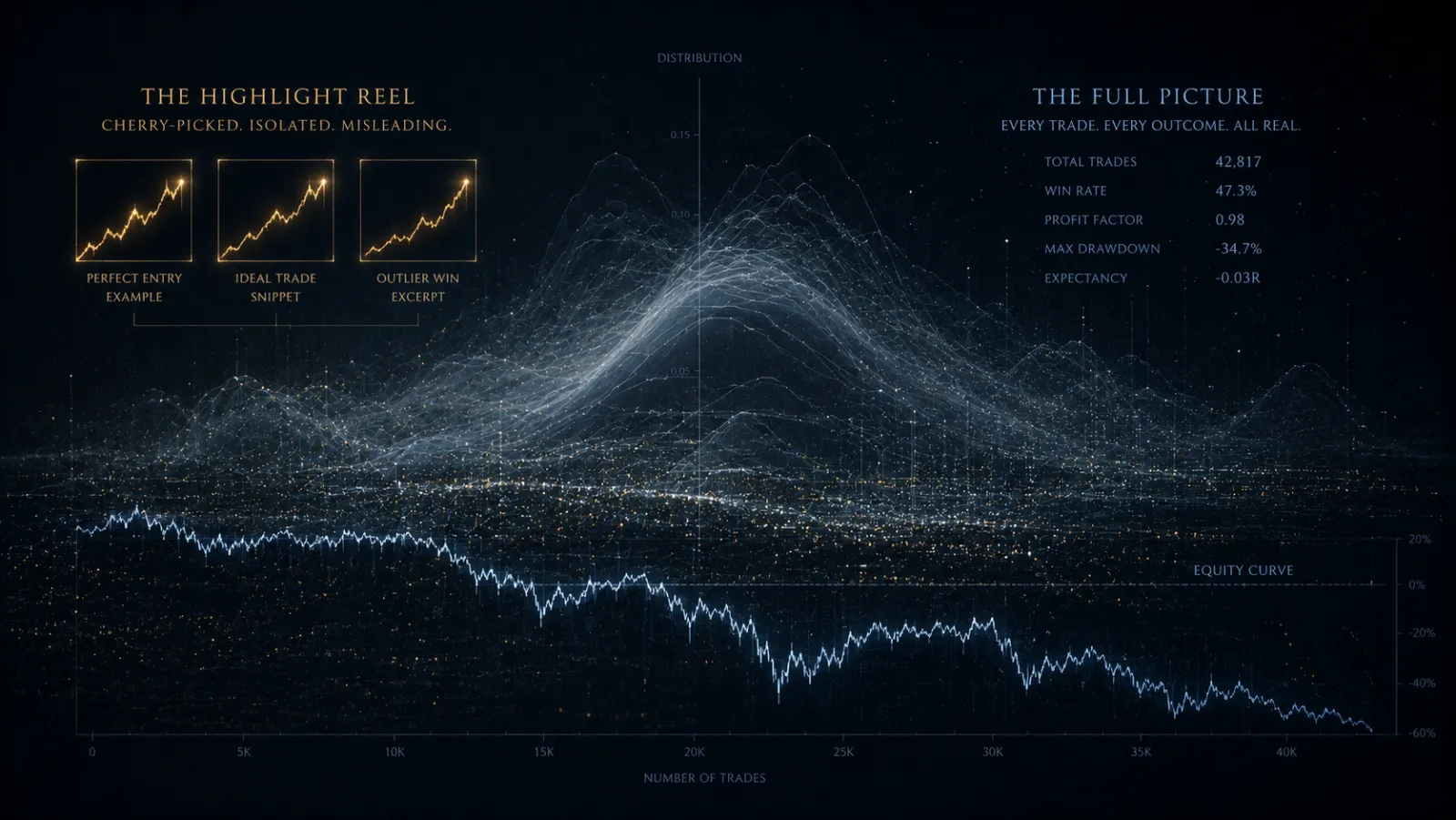

A "perfectly timed bottom" screenshot can get the blood pumping, yet it proves nothing — what you don't see are the losing trades that never got screenshotted. What actually speaks is a full set of statistics with a sample size, plus how it performs in the real market.

This is the hardest criterion in the filter from "Seeing Through Hindsight Line-Drawing": show backtest/statistical results, not single trades. This article explains why, and how to read them.

1. Why "3 perfect trades" carry no information

Picking out a few perfectly winning trades to prove your edge is the most common form of survivorship bias:

- you only see the "called it right" screenshots, because the people who called it wrong never screenshot;

- even a purely random method, given enough attempts, is bound to produce a few perfect trades;

- with no total sample size as the denominator, "won 3 trades" is meaningless — you don't know whether it's 3 wins from 3 tries or 3 wins from 30.

Any profit display with no denominator should be treated as entertainment by default.

2. The 4 metrics to watch (plus 1 denominator)

To evaluate a rule/system, you need at least this set of numbers viewed together — any one alone will mislead you:

In a sentence: "I tested this idea: PF=1.2, max drawdown 15%, win rate 42%, sample of 600 trades, especially bad in one-sided crashes." — That kind of candor is more credible than ten thousand perfect-trade screenshots.

3. Three hidden traps inside a backtest

A backtest alone isn't enough — a backtest itself can lie. The three most common ones:

Overfitting (curve-fitting)

Endlessly tuning parameters until the historical curve is perfect — reverse-carving a rule using a known future. The antidote: out-of-sample testing, robust parameter ranges. (See Part 4 of falsifiable rules)

Look-ahead bias

The backtest accidentally uses information that couldn't have been known at the time (e.g. using a candle's close to make a decision within that same candle), so results look unrealistically good.

Survivorship bias (in the data)

Backtesting only the coins/instruments still alive today automatically drops those that went to zero and delisted — the historical "landmines" are erased and the win rate is inflated.

Whoever can proactively explain how their backtest avoids these traps is the one who truly understands it.

4. The most important rule: live ≠ backtest

Even with a flawless backtest and beautiful out-of-sample results, it is still only the entry ticket, not the final verdict. Why:

- a backtest has none of the real frictions — slippage, fees, thin liquidity, API latency, fill failures in extreme conditions;

- in a backtest you have no emotions; in live trading you do;

- market structure changes — what worked in the past won't necessarily keep working.

So there is only one final courtroom: a continuous, independently checkable live record that must include losses and drawdowns. This is also why an honest performance report proactively states unrealized losses rather than only flexing peak returns.

5. Pointing this yardstick at ourselves

At this point, the right move isn't to ask you to "trust us," but to invite you to take the standard above and measure CoinTech2u yourself:

Demand the denominator and a continuous record

/live-proof reads the official system API directly every hour and shows continuous real operating data, not a curated handful of perfect trades. What you see includes the ugly parts.

Demand live trading, not a backtest

We stress live ≠ backtest; the review methodology v1.0 explicitly writes "disclose unrealized losses and drawdowns, independently verifiable by any third party" into the scoring criteria and the Auto-Fail rules.

Demand the courage to show losses

A genuine record doesn't cherry-pick. The moment it cherry-picks, it degrades into "3 perfect trades."

AI dynamic multi-strategy

Not one "holy grail" forced through every condition, but a collection of rules tested in backtest + live trading and dynamically re-weighted by market regime; funds always stay in your own exchange account (non-custodial).

If the day comes when we only dare flex the peak and won't show the drawdown, please use this article to swipe us away. Only what survives its own standard has any right to talk about credibility.

Where's the denominator? The drawdown? The continuous live record?

Next time you see a "perfectly timed bottom" screenshot, ask this one question first and you'll filter out the vast majority of noise — and you're welcome to measure us with the same question.